The Wolfram Solution for Financial Risk Management

Rapidly develop and test robust financial risk models and deploy them as interactive applications or as high-performance infrastructure components—all from one system, with one integrated workflow.

Wolfram Finance Platform is unique in offering the reliability of a mixed symbolic-numeric approach to computation, multiple switching algorithms, built-in computable financial and economic data and integrated parallel computation for scaling up performance.

The Wolfram Edge

Wolfram Finance Platform includes thousands of built-in functions that let you:

- Develop and refine analytic models for risk

- Backtesting trading strategies to check viability or stress test models to account for extreme market changes

- Access real-time trading data and perform instant analysis

- Calculate value at risk for different portfolios and time horizons

- Do straight-through processing from the trade capture to the back end

- Create new tools for calculation, graphing and modeling and deploy them to your website

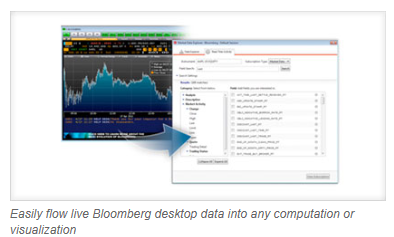

- Immediately compute with data from your existing Bloomberg feeds

- Dispatch order routing on .NET and Java platforms from one central command center

- Perform position reconciliation with online statements from the clearinghouse with XML functions

How Wolfram Compares

Does your current tool set have these advantages?

- Symbolic capabilities of time-value and bond functions allow for seamless integration with Wolfram Finance Platform's statistics framework for use in financial computations involving uncertain outcomes

- Develop, analyze, test, document and deliver custom models in a fraction of the time needed with other systems

- Get accurate results with fully automated precision control and arbitrary-precision arithmetic

All systems relying on machine arithmetic, such as Excel or Matlab, become inaccurate

- Gain accuracy and reliability by performing symbolic calculations, not just numeric ones

Matlab's built-in routines only handle numeric calculations

- Choose from procedural, functional and rule-based programming paradigms for fast development and deployment

Other computation environments use predominantly procedural languages

Key Capabilities

Wolfram Finance Platform includes thousands of built-in functions for financial computation, modeling, visualization, development and deployment, including:

- Comprehensive derivative calculations, including American, European and exotic derivative pricing, Greeks and implied volatility »

- Immediate computation on streaming data from Bloomberg »

- Symbolic and numeric time-value-of-money computations, including valuation of lump-sum amounts, annuities and continuous or discrete cash flow streams »

- Calculation of effective interest rates for continuous- or discrete-time processes and term structures »

- Bond computation functions for values, sensitivity measures, accrued interest and calendar measurements using continuous- and discrete-time coupon or interest rate processes and term structures »

- Built-in statistical analysis and probability distributions, including stable and hyperbolic distributions, plus the ability to create distributions from data or other distributions »

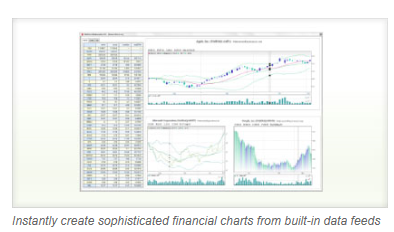

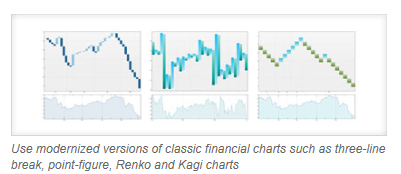

- State-of-the-art data visualization with scaling functions; paired bar charts and histograms; and finance-specific charts like candlestick, point and figure, Kagi and more »

- Immediately create highly customized interactive financial charts using 100 built-in financial indicators »

- Integrated GPU computation, with CUDA and OpenCL support and external dynamic libraries for fast, efficient execution

- Built-in financial data, including current and historic market data, plus programmatic and interactive access to financial and economic data from Wolfram|Alpha

- Automated report creation, PDF export and interactive deployment with Wolfram Player or webMathematica to deliver results to management or clients

- Seamless integration of R, C and C++ code into your workflow.

- Advanced IDE for a rapid development workflow for computation-centric applications »

- Integrated random processes, signal processing and graphs and networks functionality

- Efficient random number generation for Markov chain Monte Carlo (MCMC) techniques »

- Import and export all common data formats, including XML, XLS, CSV and TSV or use Mathematica Link for Excel to run Mathematica and Excel side by side

- Use highly customizable interactive gauges to convey spreadsheets' worth of information with a single glance »